As readers of our favorite sustainability newsletter — Trellis Briefing — know well, staying current in this fast-changing field isn’t enough. The most successful professionals stay ahead. That means tracking each new regulation and all emerging tech, not to mention shifts in consumer demand and a crisis that changes daily.

Trellis Briefing offers a unique blend of management advice, regulatory updates, corporate case studies and more makes it a must read for anyone in the industry.

But we’re the first to acknowledge that there are more than a few other newsletters in our sector that we like — and read.

Whether you skim these “subscribes” as you sip your morning coffee or save them for a leisurely weekend scroll, they will keep you plugged into both what is and what’s next.

If you want clean energy news that cuts to the chase …

Axios Energy takes the ever-changing world of sustainability, from policy moves to corporate shifts, and breaks it all down into bite-size, inbox friendly reports. From renewables to grid tech, Axios Energy is a must for anyone tracking the business of decarbonization. As you peruse their website, you’ll happily note that each read takes no more than three minutes. That’s shorter than the time it takes to brew a cup of joe.

If you want your sustainability news served with a side of global depth and data …

Few sustainability news outlets combine breadth and rigor like Bloomberg Green. From deep dives into the financial side of climate action to people-first stories of adaptation and innovation, its reporting highlights how environmental action is reshaping the economy, politics and culture worldwide. You might find your next sustainability breakthrough within its (digital) pages.

If you want to follow the money …

Perfect for investors and founders, Climate Tech VC has proven itself a global voice in the business of sustainability. The weekly newsletter tracks deals, trends and venture movement across the industry, pairing data with insight to create the perfect window into where climate capital is flowing.

If you want to know what’s really happening in Washington …

While policies might not always make for attention-grabbing headlines, we’re never ones to discount the importance of staying informed. We believe policy reporting can and should be enjoyable, which is whyPower Switch from Politico is on our list. The newsletter delivers sharp, inside-the-Beltway reporting on the political forces shaping today and tomorrow’s environmental scene.

If you want your climate journalism to replace your daily doomscroll …

Heatmap does what few sustainability publications do: makes its readers laugh. It has carved a niche in the sector that is both entertaining and informative, covering everything from the cultural impact of sustainability to the politics of electrification. The newsletter delivers punchy climate coverage with bright colors, savvy pop culture references and jokes aplenty.

If you want energy media that connects the dots …

Few outlets capture the pulse of clean energy, renewables and the climate revolution like Canary Media. This nonprofit newsroom provides a clear-eyed look at decarbonization — from solar wind to electrification — while explaining what works, what doesn’t and why. The newsletter is committed to bringing solutions to a sector full of questions, connecting policy to technology and technology to people.

If you want clarity in a feed full of headlines …

Carbon Brief offers its readers a daily breakdown of the biggest stories in sustainability while maintaining a voice that’s clear and factual. If you’re looking for crisp, data-driven stories that prioritize comprehension over haste, you’re in the right place. With charts that cut through the noise, data that doesn’t distort and analysis that connects policy and science, the newsletter delivers evidence-based journalism that keeps readers thoroughly informed without overwhelming them.

If you want to hear unique individual voices …

Climate activist legend Bill McKibben, co-founder of 350.org, brings decades of environmental insight to his Substack, The Crucial Years. With nearly 100,000 subscribers, it reflects on grassroots campaigns, policy battles and big-picture climate trends. Other notable climate apostles: Michael Thomas, whose newsletter Distilledboasts 16,000 subscribers, and Emily Atkin, whose 145,000-subscriber-strong HEATEDwas termed “impassioned [and] deeply reported” by New York Magazine.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-10-24 10:14:002025-10-24 18:08:3210 (other) newsletters to make your scroll more sustainable

As readers of our favorite sustainability newsletter — Trellis Briefing — know well, staying current in this fast-changing field isn’t enough. The most successful professionals stay ahead. That means tracking each new regulation and all emerging tech, not to mention shifts in consumer demand and a crisis that changes daily.

Trellis Briefing offers a unique blend of management advice, regulatory updates, corporate case studies and more makes it a must read for anyone in the industry.

But we’re the first to acknowledge that there are more than a few other newsletters in our sector that we like — and read.

Whether you skim these “subscribes” as you sip your morning coffee or save them for a leisurely weekend scroll, they will keep you plugged into both what is and what’s next.

If you want clean energy news that cuts to the chase …

Axios Energy takes the ever-changing world of sustainability, from policy moves to corporate shifts, and breaks it all down into bite-size, inbox friendly reports. From renewables to grid tech, Axios Energy is a must for anyone tracking the business of decarbonization. As you peruse their website, you’ll happily note that each read takes no more than three minutes. That’s shorter than the time it takes to brew a cup of joe.

If you want your sustainability news served with a side of global depth and data …

Few sustainability news outlets combine breadth and rigor like Bloomberg Green. From deep dives into the financial side of climate action to people-first stories of adaptation and innovation, its reporting highlights how environmental action is reshaping the economy, politics and culture worldwide. You might find your next sustainability breakthrough within its (digital) pages.

If you want to follow the money …

Perfect for investors and founders, Climate Tech VC has proven itself a global voice in the business of sustainability. The weekly newsletter tracks deals, trends and venture movement across the industry, pairing data with insight to create the perfect window into where climate capital is flowing.

If you want to know what’s really happening in Washington …

While policies might not always make for attention-grabbing headlines, we’re never ones to discount the importance of staying informed. We believe policy reporting can and should be enjoyable, which is whyPower Switch from Politico is on our list. The newsletter delivers sharp, inside-the-Beltway reporting on the political forces shaping today and tomorrow’s environmental scene.

If you want your climate journalism to replace your daily doomscroll …

Heatmap does what few sustainability publications do: makes its readers laugh. It has carved a niche in the sector that is both entertaining and informative, covering everything from the cultural impact of sustainability to the politics of electrification. The newsletter delivers punchy climate coverage with bright colors, savvy pop culture references and jokes aplenty.

If you want energy media that connects the dots …

Few outlets capture the pulse of clean energy, renewables and the climate revolution like Canary Media. This nonprofit newsroom provides a clear-eyed look at decarbonization — from solar wind to electrification — while explaining what works, what doesn’t and why. The newsletter is committed to bringing solutions to a sector full of questions, connecting policy to technology and technology to people.

If you want clarity in a feed full of headlines …

Carbon Brief offers its readers a daily breakdown of the biggest stories in sustainability while maintaining a voice that’s clear and factual. If you’re looking for crisp, data-driven stories that prioritize comprehension over haste, you’re in the right place. With charts that cut through the noise, data that doesn’t distort and analysis that connects policy and science, the newsletter delivers evidence-based journalism that keeps readers thoroughly informed without overwhelming them.

If you want to hear unique individual voices …

Climate activist legend Bill McKibben, co-founder of 350.org, brings decades of environmental insight to his Substack, The Crucial Years. With nearly 100,000 subscribers, it reflects on grassroots campaigns, policy battles and big-picture climate trends. Other notable climate apostles: Michael Thomas, whose newsletter Distilledboasts 16,000 subscribers, and Emily Atkin, whose 145,000-subscriber-strong HEATEDwas termed “impassioned [and] deeply reported” by New York Magazine.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-10-24 10:14:002025-10-26 18:08:2710 (other) newsletters to make your scroll more sustainable

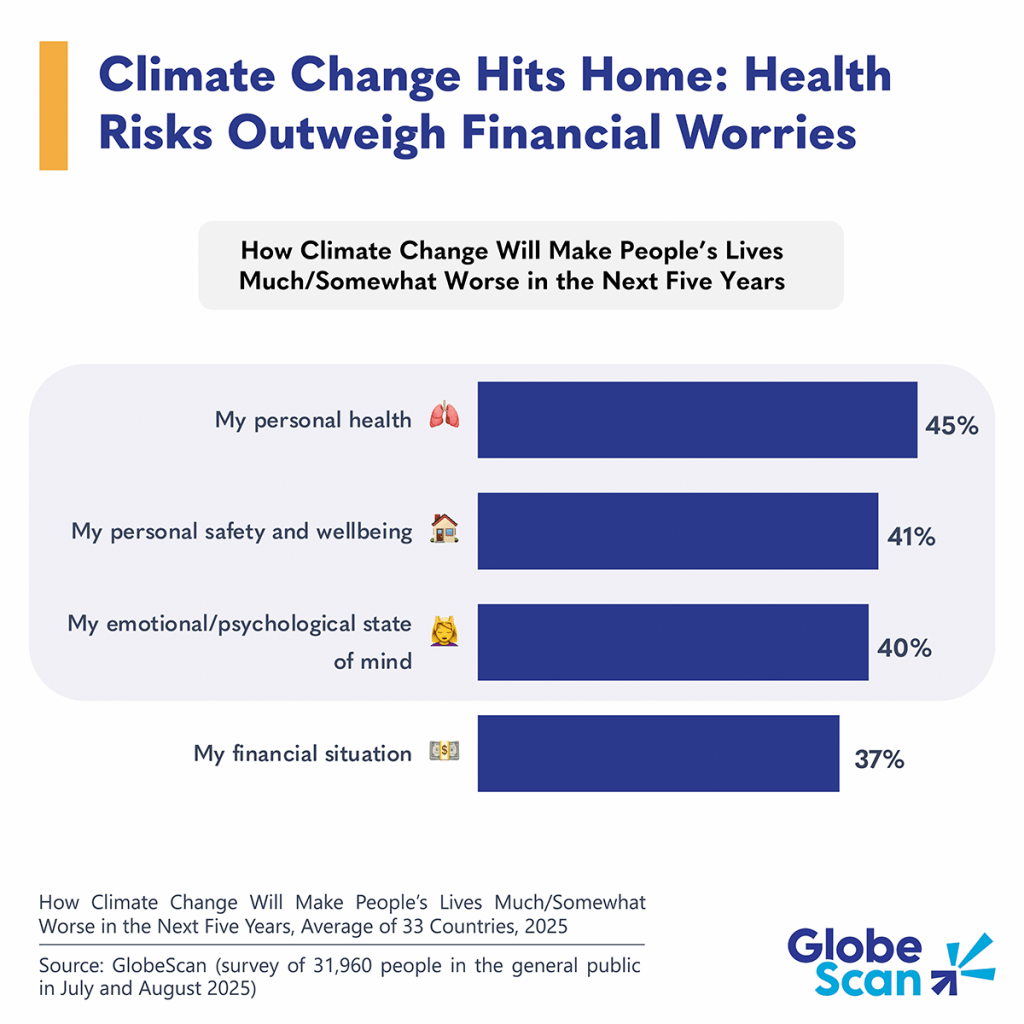

While there are many personal impacts of climate change, new data shows people are most concerned about one: their health.

Globally, 45 percent of people believe climate change will negatively affect their personal health in the next five years, making health a potential rallying point for climate action, according to Trellis data partner GlobeScan. Additionally, 41 percent expect climate change to worsen their personal safety and well-being, while 40 percent foresee a decline in their emotional and psychological state, highlighting the deep and multifaceted anxieties people associate with climate disruption.

Financial vulnerability is also a concern, although less so than physical or emotional impacts, with 37 percent of respondents believing their financial situation will deteriorate due to climate change. This reinforces the tension between recognizing climate risks and hesitating to make financial sacrifices to address them.

What this means

Health concerns are emerging as a strong personal link to climate change and a major opportunity to drive action. People are more worried about the effects of climate change on their health and well-being than on their finances, making health a powerful and universal motivator. Framing climate change as a public health issue shifts the conversation from distant environmental threats to immediate personal impacts such as cleaner air, safer water and reduced risk of disease. Highlighting these tangible benefits can make climate action more relatable and widely supported, helping to engage people beyond traditional environmental audiences.

Based on GlobeScan’s Societal Shift project, which surveyed nearly 32,000 people in 33 countries in July and August 2025.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-10-24 10:00:002025-10-24 18:10:11Nearly 50 percent of people expect climate change to harm their health within 5 years

When the sustainability team at the outdoor clothing company Patagonia began developing a science-based target, it knew it faced a formidable challenge.

Upwards of 85 percent of Patagonia’s emissions are generated by suppliers. The company’s goal, validated by the Science Based Targets initiative in 2023, commits it to cutting those emissions by 55 percent by 2030. Yet Patagonia’s supply-chain network contains hundreds of companies, and it can exert only limited influence over each.

Consider a supplier that dyes fabrics. Patagonia might want to help the company replace a fossil fuel boiler with an electric version — a costly project that would take years to complete. But Patagonia’s purchases may account for 1 or 2 percent of the supplier’s business. Why would Patagonia fund the change only to see the large majority of the emissions savings flow to the supplier’s other customers?

The solution was an innovative means of accounting for the benefits of such an intervention. Patagonia began work on the approach internally but soon teamed up with the Advanced and Indirect Mitigation (AIM) Platform, a cross-sector initiative crafting guidelines for what is known as insetting or value-chain intervention. The guidelines — currently being tested by H&M Group, Heidelberg Materials, Netflix and others — entered a second pilot phase last month and are due to be finalized next spring.

Patagonia has in fact signed a contract to replace a boiler used by a supplier in Taiwan. The supplier is currently monitoring its business-as-usual emissions, which will serve as a baseline against which to assess future savings. When the new boiler is in place, Patagonia will receive credits, known as environmental attribute certificates (EACs), that can be netted against emissions from dyeing across its Scope 3 inventory. The company expects to receive credits for 27,500 metric tons of carbon dioxide equivalent from the project this year.

Countless other projects could be catalyzed if the AIM Platform can develop trusted rules for guiding this and other value-chain investments. Pilot testers are using the rules to oversee funding for projects to purchase renewable energy on behalf of suppliers and customers, enable the switch to sustainable maritime fuels and reduce on-farm emissions.

“We see platforms like AIM as essential for scaling high-quality climate solutions across industries,” said Taylor Gries, sustainability manager at REI, another pilot tester.

One area the guidelines will cover is how credits are allocated. Kim Drenner, Patagonia’s head of environmental impact, said each contract has a defined period, ranging from 5 to 15 years, during which the company funding the work would receive credits covering all the emissions savings. Patagonia gauges the value of potential interventions by estimating the cost per ton of avoided carbon dioxide emissions. “That can range from around $90 a ton, all the way up to $300,” said Drenner.

Negotiating agreements with suppliers can be challenging, in part because relationships with other customers can be affected. Because Patagonia is netting all the savings against its emissions inventory, none of the supplier’s other customers can claim similar emissions savings. To guard against such double counting, the contract prohibits the supplier from sharing emissions data in a way that customers have come to expect.

“We’re coming in and saying, ‘We’re going to buy these EACs from you; you can’t send that data,’” said Drenner.

This second pilot phase for AIM will focus on guidelines for assessing the quality of an intervention and how companies should measure the emissions savings. It follows an earlier test of rules for determining whether an intervention is part of a company’s value chain, and hence part of its Scope 3 emissions. The platform is a joint initiative of three non-profits: Gold Standard, the Center for Green Market Activation and the Center for Climate and Energy Solutions.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-10-24 10:00:002025-10-24 18:10:12Patagonia pilot project shows how to catalyze climate finance across economy

Rebecca White grew up in West Texas cotton country, so she understands firsthand how climate stresses and volatile markets threaten the crop. Now, as chief product officer of the agtech startup Avalo, she hopes to help future-proof cotton from seed to field.

Avalo uses machine learning to accelerate what Gregor Mendel once did with peas. Its AI analyzes plant genomes and recommends which plants to crossbreed for desired fiber traits, sometimes even multiple qualities at once. In the process, Avalo says it enhances genetic diversity and helps farmers generate value through low-chemical, regenerative practices.

The pitch to fashion brands and mills: fibers tailored for softness, breathability, dye-readiness and other properties. “When we look at genetics for our seeds, we’re talking to spinners, millers and brands about what is important in the fiber characteristics for them,” White said.

White expressed hope for helping farmers stressed by a variety of factors, including the decline of cotton in fashion, capricious weather patterns worsened by climate change and volatile tariff policies. “If we’re not taking care of farmers, then they’re not going to farm anymore,” she said.

Competitors

Avalo raised $11 million in a Series A round in March, part of about $15 million total raised to date. (It also has support from Coca-Cola Ventures for sugar cane genetics.) The amount is modest next to peers in the biotech-for-ag space:

Indigo Ag (Boston) has raised roughly $1.5 billion, including a large 2023 round with Google Ventures participation, to track and monetize regenerative agriculture practices for multiple crops.

Puna Bio (Buenos Aires and San Francisco) makes microbial seed coatings from extremophile organisms to boost yields. Its $25.7 million in funding includes support from the Gates Foundation.

Galy (Boston) cultures cotton and other fibers in bioreactors, backed by $65.9 million in funding, including a Series B raise from Breakthrough Energy Ventures in 2024.

White says Avalo’s focus on using genetics to help farmers maximize yields and build soil health can ultimately complement other technologies such as those of Indigo Ag and Puna Bio.

“It’s great that there are those kinds of initiatives, but it’s still high risk,” said Margaret Bishop, an assistant professor at the New School in New York City. “You’ve got to have the investors and build out the supply chain.”

In the field

Avalo aims to enable sustainable farming practices already familiar to growers in arid regions around Lubbock. Delivering improved fiber quality with plant strains suited to local conditions could help farmers earn more for lower-emission cotton, while also assisting mills and brands to cut Scope 3 supply-chain emissions.

Unlike traditional ag models that sell seeds plus chemical inputs, Avalo’s team wants to work toward a future with fewer herbicides and pesticides, developing varieties with built-in resistance.

Although its seeds start in a lab, Avalo relies on open-air field trials, where bees pollinate plants. “We’re really trying to bring genetic diversity back into the fold, because traditional breeding programs tend to weed diversity out in an attempt to keep things simple and more streamlined,” said Avalo Chief Marketing Officer Nick Schwanz.

The company taps into public seed banks and private collections to study more than 500 cotton varieties. These include both wild and “feral” types, i.e. onetime commercial strains that naturalized over decades.

“The oldest one that we have is from the 1920s,” White said. “We put them all together in various different locations, and we see how they do in those different environments, and that helps us interpret the underlying genetic information.”

Natural and synthetic pressures

In fashion, cotton and polyester have traded places in dominance over the past 60 years. Polyester and other fossil-based synthetics now make up about 59 percent of the global fiber market, while cotton accounts for roughly 19 percent, according to the Textile Exchange 2025 Materials Market Report.

Virgin synthetics generally carry a higher greenhouse-gas footprint, but cotton’s cultivation uses more land and water. Cotton-growing regions in the U.S., India, Brazil and Pakistan face future uncertainty from increased droughts, rains and flooding.

Sustainability advocates argue that retailers and brands must rethink how they work with farmers, supporting transitions to regenerative and climate-resilient cotton. The Sustainable Cotton Challenge led by Textile Exchange has gathered 138 brands, from Levi Strauss to Kering, committed to sourcing certified environmentally responsible cotton by the end of 2025. Yet only about 22 percent of participating brands met that goal by the end of 2024.

Avalo positions itself as the bridge between regenerative farming and brands’ sustainability ambitions, aiming to give both sides a shared language and measurable results.

“Farmers know what happens to their cotton up to the point where it leaves the warehouse,” White said. “They produce it, they harvest it. It goes to a gin, it gets bailed, and then it goes to the warehouse, and then it’s sort of off in the ether for them.”

The opposite is true for the brands, who only tend to see the cotton after it lands at the spinner. “The brands are closer together in a perspective of sustainability with farmers than they think that they are,” she added. “The more that we can bring that understanding together, I think the more successful programs like ours will be.”

“It’s super early to know how much that’s going to speed up the development of new seeds, but really exciting if they can,” said Debra Guo, the cotton and crops lead at the Textile Exchange.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-10-24 10:00:002025-10-24 18:10:14Avalo using AI to future-proof cotton

PepsiCo, like many other companies with environmental commitments set or reset in the 2020 timeframe, downgraded some goals within its 2025 sustainability reporting cycle — extending the deadline for its long-term net-zero commitment from 2040 to 2050.

PepsiCo, in contrast, offers deep detail about its revisions and the thinking that drove them in its comprehensive online reporting hub, updated in August.

“We wanted to be as transparent as possible, because transparency plus accountability equals trust,” said PepsiCo Chief Sustainability Officer Jim Andrew, during the latest episode of Climate Pioneers, our series featuring innovators and leaders shaping the corporate climate movement.

“If you wanted to wade through the footnotes and understand the logic, we tried to make that as clear as possible,” he said. “And then we also had a very simple summary, so if you wanted to hit the high points, you could also do that.”

It takes a system

PepsiCo reviews all sustainability goals comprehensively every four to five years, not just as a reporting exercise but to understand what should be changed. Each commitment was evaluated separately to better understand what was driving or prohibiting progress. The goal: learn and adjust.

“If we haven’t learned anything in four or five years, then shame on us because certainly a lot of things look different,” said Andrew, who reports to PepsiCo’s CEO and meets with his counterparts in the C-suite at least monthly.

The prevailing rationale for many downgrades PepsiCo describes in its disclosures — including the extension of its net-zero commitment by 10 years and its retreat from a 2030 pledge to cut virgin plastic consumption by 20 percent — is the lack of systemic support for those ambitions, according to Andrew.

“Overall, there’s things that individual companies can do, and there’s a range of aspirations and commitments to doing those things by different types of companies, but there is also a tremendous amount that’s dependent on the systems that we’re all a part of,” he said.

Because the majority of national emissions reduction commitments are pegged to 2050 or later, it’s difficult for any one multinational corporation to accomplish the same thing more quickly.

“You can’t move a system as big as ours around the world faster than the whole world is moving,” Andrew said. “It’s just unrealistic. So we said 2050 is much better aligned with what the world is doing.” The new targets are also aligned with the goal of keeping global temperatures below 1.5 degrees Celsius, whereas the previous ones were set for a 2 degrees change.

Point of influence: regenerative agriculture

Not all of PepsiCo’s revisions reflect a belief that progress will be slower. The $92 billion company — which gets roughly 60 percent of its revenue from food brands including Lay’s and Quaker Oats — made its targets for sourcing ingredients tougher to achieve by increasing a commitment to buying from farms using regenerative agriculture to 10 million acres by 2030, up from 7 million. As of its latest progress update in August, it had achieved 3.5 million acres.

The new goal represents well over half of the land required to grow around 50 major crops — notably oats, potatoes and corn — needed for PepsiCo’s products.

The economic crisis in farming is one reason for this heightened focus, Andrew acknowledged, because regenerative agriculture provides an opportunity for farmers to reframe their value proposition. It also gives PepsiCo a role in that transition.

Just as important for PepsiCo’s confidence in making the shift was the supportive network of corporate partners that it collaborates with to develop initiatives and incentives for the roughly 300,000 farmers in the conglomerate’s agricultural chain, which spans 60 countries.

It’s important to provide farmers financial incentives, technical advice and cultural support to bridge the transition to regenerative agriculture practices, which usually takes three to four years. In many tight-knit U.S. farming communities, regenerative agriculture is still seen as an unorthodox choice that neighbors might question. PepsiCo builds provisions for this support into contracts with farmers that are willing to make the commitment.

“I think that many farmers know that moving to regenerative practices is better for their farms, better for the soil,” Andrew said.

Methods such as planting cover crops to protect soil erosion and decreasing fertilizer usage lower costs for the same yield and improve resilience. “You end up better off, but you’ve got to get from here to there,” he said.

Watch the whole Jim Andrew interview. Look for more coverage of this conversation and other Climate Pioneers features by signing up for Trellis Briefing.

This week, some 2,000 folks — businesspeople, NGO leaders, academics and others — are gathering in Bentonville, Arkansas, to mark the 20th anniversary of a seminal moment in the short history of sustainable business: a speech by the CEO of Walmart.

On Oct. 23, 2005, Lee Scott stood on the stage of the auditorium in Walmart’s Home Office to talk about “21st Century Leadership.” In a rare moment, the famously improvisational CEO held a script in his hands and read it word for word to ensure every sentiment was well articulated.

In the speech, Scott acknowledged the breadth of his company’s challenges, referencing “jobs, healthcare, community involvement, product sourcing, diversity, environmental impact: all the issues that we’ve been dealing with historically from a defensive posture.”

All of them, he said, “represent gateways for Walmart in becoming the most competitive and innovative company in the world.”

He reframed Walmart’s role, pledging ambitious sustainability leadership, and linked social and environmental stewardship with business efficiency while committing to workforce improvements.

Lasting influence

Scott committed the company to three ambitious environmental goals:

Obtain 100 percent of the company’s energy from renewable sources

Create zero waste

Sell products that “sustain our resources and environment”

Walmart views its sustainability journey through three distinct eras. Source: Walmart

“These goals are both ambitious and aspirational, and I’m not sure how to achieve them, at least not yet,” Scott said. “This obviously will take some time.”

Those three goals set in motion myriad initiatives, partnerships and collaborations that have demonstrably moved the needle on Walmart’s footprint and have influenced other companies — suppliers, competitors and others — to follow along.

Over the past few weeks, I’ve spoken to nearly a dozen current and former Walmart employees as well as activists, academics and other observers. My quest: to assess the impact and influence of Scott’s speech, including its three sustainability commitments.

(For more backstory behind the speech, see this 2015 piece marking its 10-year anniversary.)

From pariah to partnerships

Until Scott’s speech, Walmart had little to do with sustainability. “We were doing our best to stop legislation that was warranted about runoff on parking lots from fertilizer,” Andy Ruben, who’d become Walmart’s first chief sustainability officer a year earlier, told me. “That’s what was going on in sustainability. It was a ticking time bomb of one more black eye the company could experience.” Everything else had been on the table, he said, such as the company’s impact on Main Street and on its labor force.

“But not this.”

Elizabeth Sturcken, vice president for net zero ambition and action at the Environmental Defense Fund, who has engaged with Walmart for nearly two decades, put it more bluntly: “They were a pariah.”

The year 2005 had already been a pivotal one for corporate sustainability. A few months earlier, for example, GE had launched Ecomagination. Other executives — Mark Tercek at Goldman Sachs, John Browne at British Petroleum, Jorma Ollila at Nokia, Jeff Immelt at GE, Chad Holliday at Dupont, Jim Rogers at Duke Energy and Bill Ford at Ford — were making headlines for their commitments.

For Scott, the time seemed right for a bold move.

‘A generous C’

So, how has the company fared? Scott’s three goals are still largely works in progress. Here are some stats, most culled from the company’s fiscal 2025 ESG Report:

48.5 percent of Walmart’s global electricity needs are supplied by renewable energy.

43.3 million acres of land has been “more sustainably managed, protected or restored.”

Its Scope 1 and 2 emissions are 18.1 percent lower than the 2015 baseline.

The company’s Scope 3 emissions have ratcheted up about 4 percent over the past two years, though its intensity — emissions per dollar of revenue — declined about 6 percent over that period.

83.5 percent of Walmart’s global operational waste has been diverted from landfills and incineration.

82.6 percent of its private brand plastic packaging is “designed for recycling.”

95.1 percent of Walmart U.S. fresh and frozen seafood, both wild-caught and farmed, was reported by suppliers as “more sustainably sourced.”

True, some of this language — “more sustainably,” for instance — is squishy at best. And transparency is sometimes lacking. For example, Project Gigaton, launched in 2017, blends reduced, avoided and sequestered emissions in its reporting and does not fully delineate each category with transparent, publicly verifiable breakdowns.

Still, these data points cover a two-decade period in which the company’s global revenue, adjusted for inflation, grew 44 percent, to $681 billion for fiscal 2025. That means that even as the company grew, several of its impacts didn’t.

Scott’s speech planted the seeds for a bumper crop of company initiatives. Some, such as its Sustainability Index (to establish a single source of data for evaluating the sustainability of products) and its Sustainable Value Networks (collaborations with suppliers, nonprofits and other stakeholders to improve product environmental performance) became part of the fabric, ran their course or morphed into other initiatives. Others, such as Project Gigaton, with the goal of removing a billion metric tons of greenhouse gases from Walmart’s supply chain, continue to be showcased by the company.

As graded by Jon Johnson, a professor in the Walton College of Business at the University of Arkansas, who’s been following the company for decades, “I would give them an A or A-minus on their waste and energy goals. I give them a C on their product goals, and that would be a generous C.”

Source: Walmart

Listening to critics

Assessing Walmart’s impact epitomizes the glass-half-full/half-empty challenge of sustainable business: Should a company be assessed on progress made or on work still to be done? That debate is particularly relevant to some of the world’s largest brands — McDonald’s, Amazon, Microsoft and others. For critics, it can be more rewarding to knock these companies’ failings — or fault the capitalist system within which they operate — than to acknowledge their achievements, however imperfect.

(This dilemma is highlighted in our Chasing Net Zero series, which examines companies’ progress, or lack thereof, in meeting emissions-reduction goals.)

In the case of Walmart, there’s been plenty to criticize: its low wages, which can cost taxpayers by increasing the need for public assistance programs among employees; an anti-union stance that chills worker organizing and protest; weak traceability of deforestation in its supply chain; packaging and waste goals that rely on voluntary supplier actions; chemical safety transparency gaps across its sprawling private-label and supplier networks. The list of perceived shortcomings goes on.

“We’re not a perfect company,” acknowledged Kathleen McLaughlin, Walmart’s current CSO. “One of the things that is pretty deep at Walmart, though, is really listening to everybody, to critics and to stakeholders.”

Ken Cook agrees. As president and co-founder of the Environmental Working Group (EWG), an advocacy group that focuses on environmental and public health issues, he has been engaging Walmart for much of the past two decades, with notable successes. For example, a 2014 EWG campaign led to Walmart requiring suppliers to limit or eliminate a set of “priority chemicals” in products it sells, particularly in household cleaning, personal care and beauty and cosmetic items. The company also agreed to recognize EWG Verified as part of its sustainability standards, meaning vetted products would be listed as complying with Walmart’s “Built for Better” criteria.

Cook noted that Walmart’s scale gave NGO standards such as his meaningful reach. “EWG is not interested in things that don’t make landscape-level changes,” he said. “This is what Walmart has provided.”

Another supportive group is EDF, which in 2007 opened an office in Bentonville adjacent to Walmart headquarters, the first NGO (and still one of the few) to do so.

Sturcken cited Walmart’s 2017 chemical footprint goal, aimed at restricting over 2,700 harmful chemicals in household products, as one example of the retailer’s influence. “You got very real ripple effects throughout the entire industry,” she said, citing Target and Dollar General as examples of retailers that followed suit.

“These past 20 years of work that Walmart has done on sustainability has transformed a generation of business,” Sturcken said. “They prioritized and democratized sustainability.”

Still, she added: “Walmart is not a sustainable company. They’re falling behind in their operational goals. And they’ve always had a big challenge and needed to do so much more on product sustainability and their supply chain.”

Mixed results on sustainable products

For Johnson, like for so many others, Scott’s speech “made the possibility that companies taking sustainability seriously could have substantial impact beyond government regulation,” he said. In 2009, Johnson co-founded The Sustainability Consortium, an ambitious effort to measure and standardize product impacts across consumer goods supply chains, launched in collaboration with Walmart.

That quest — the third of Walmart’s original goals, to sell more sustainable products — is arguably the most ambitious and the least fulfilled. Walmart has never adequately raised the subject in the buying rooms, where its buyers meet daily with suppliers’ representatives, Johnson said.

“Our task was to create a measurement reporting system for consumer goods,” he explained. He and his team at The Sustainability Consortium developed metrics that assess the impacts of products throughout their life cycle, “a good scientifically grounded system for understanding what those claims actually mean and whether they are meaningful,” as he put it.

“Walmart never used that information to make procurement decisions at any scale that had the effect we were hoping it would,” he added.

One issue may have been failing to prioritize the most environmentally problematic products. “We probably looked at every product as an opportunity to make it better,” Matt Kistler, Walmart’s second CSO, told me. “And there’s some products where the juice was not worth the squeeze. We should have been more focused.”

There were successes. In 2008, for example, Walmart phased out large bottles of laundry detergent, replacing them with compact versions that are now the industry standard, saving shelf space, labor, shipping emissions and costs. Compact fluorescent light bulbs were another bright spot. In late 2006, the company announced a goal to sell 100 million of them by the end of 2007 to save consumers money and reduce emissions, a goal achieved ahead of schedule.

But other products and packaging remain stubborn — plastics, in particular. Although Walmart has set ambitious targets, actual reduction in plastic packaging weight has been challenging, especially given business growth and the addition of packaging types, such as those used in e-commerce.

Can system transformation be scaled?

Taking the full measure of Walmart’s impacts turns out to be a complicated affair. For each shortcoming, there are unheralded successes.

For example, “We were late and slow on paying our people what they needed,” said Leslie Dach, who in 2013 stepped down from his role as Walmart’s executive vice president, where he oversaw sustainability, among other things. “I think we could have done more about people’s way of living.”

At the same time, he pointed out, “We followed a progressive agenda in sustainability, in women’s economic empowerment, in bringing manufacturing back from China,” including a 2013 initiative to reshore $50 billion worth of manufactured goods from that country.

Other initiatives have received relatively little media attention. One is the Gigaton PPA, which in part provides training and resources to help suppliers invest in renewable energy, including helping them reduce barriers to sourcing renewables. Walmart has worked with HSBC to launch a sustainable supply chain finance program to offer early payment to suppliers that set science-based targets or clear a CDP score threshold. Its Circular Connector, launched in 2022, aims to accelerate innovation in sustainable and circular packaging.

All of these and more, says CSO McLaughlin, are part of a bigger change the company is undergoing.

“The easier things have been tackled,” she said. “We’re now in the throes of true system transformation, and that’s hard work. At the heart of it, we’re talking about shifting the way that system functions so that it is elevating and regenerating people and the planet. That has to be the way that it works or it’s not sustainable.”

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-10-23 07:53:002025-10-23 18:09:4920 years later, assessing the impact of a Walmart CEO’s ‘gutsy’ sustainability speech

The opinions expressed here by Trellis expert contributors are their own, not those of Trellis.

Whether companies like to admit it or not, trade rules and sustainability targets are integrated into the same business operations that purchase orders, calendars and factory lines are. They influence the same yarn, fabric, cartons and bookings. So when they’re included in a single operating plan, execution becomes clearer and issues are more easily resolved.

Split them into unrelated sourcing and environmental programs and you pay twice. A tariff change that reroutes a fabric from, say, China to Vietnam, also affects emissions, labor exposure and paperwork. A disclosure rule altering fiber content can trigger origin rules and higher duty rates, as could be the case under the Uyghur Forced Labor Prevention Act. The levers move together regardless whether you plan for it.

By consolidating operations, sourcing and sustainability into one plan, companies are able to share data, set common milestones and have one bill of materials. If you keep the specifications stable, track changes centrally and document the process as you develop the product, you’ll end up with reduced surprises and lower airfreight costs.

As you work to devise a streamlined plan, here are five aspects of apparel operations to consider.

Policy is an operating variable

A tariff isn’t just a footnote; it determines where spinning, knitting, dyeing and sewing take place. Moving production to a different country changes lead times, grid mix, defect risk and vendor reliability. And price is only the beginning of the ripple effect.

When rules change, markets rush toward the same “safe harbor.” Capacity decreases, schedules become unstable and quality declines as overbooked plants spread work across more lines and shifts. In these conditions, emergency freight acts as a pressure valve, but emissions increase in response, as geographic distances could result in a larger carbon footprint.

The lesson: Plan for volatility and don’t just react to it. Double-qualify critical inputs, maintain a second finishing route and keep pre-negotiated terms ready. Clear, predictable rules attract investment and customers; whipsaw policies push those away. Treat policy like weather: always have a Plan B you can execute this quarter, not next year.

Don’t brush off disclosures

Audits rely on records, not marketing. Indeed, effective business operations mandate lot-level traceability, credible fiber origin and chain-of-custody proof that can withstand sampling. If you can’t provide receipts, process travelers, test results and pack-out records matching the goods, reconstruction will be slow and expensive.

It’s also important to use a single workflow for production, quality and chain of custody. When documentation accompanies the order — from intake to pack-out — the records in the file match the product in the box. If compliance is stored in a separate folder, the trail is already broken.

The lesson: Brands should focus on contracting for evidence rather than marketing claims. Regulators should establish and publish acceptance criteria and identify credible systems across markets. Clear rules and expectations reduce friction and channel capital toward meaningful upgrades, not superficial efforts.

Consider where work happens

Significant supply chain costs lie in energy, process chemistry and logistics, while policy influences all three. Moving the origin alters the grid mix. Tightening origin rules introduces steps that affect transportation and packaging, while changing a dye class affects wastewater and worker exposure.

There’s no “sustainable” country, but there are sustainable networks. The resilient model is a close-knit group of capable partners following standard processes, with automation where it’s effective and measurement that continues nonstop. Documents flow with the shipments. Exceptions are identified early while they’re still inexpensive.

The lesson: Target policies with meaningful outcomes by consistently and digitally verifying renewable energy, wastewater efficiency and worker safety. Reward plants that invest and remain committed to sustainable production. Stop funding constant border-hopping that wastes time, money and credibility.

Be mindful of fibers and the proof gap

Fiber debates — cotton versus polyester, recycled versus virgin, and so forth — stir up controversy when claims exceed reality. Trade rules specify origin, but blends make labeling and duties more complicated. The basic rule is clear: If you can’t prove it, don’t claim it.

That’s why it’s important to reduce variation to make proof repeatable. Standardize blends, dyestuffs and finishes when possible and minimize one-off recipes that require new documentation each season. Fewer, better inputs scale; sprawling menus don’t.

The lesson: Pair traceability tools with a small, trusted group of mills and factories. Complexity is where quality and compliance often break down. Each new variation becomes a failure point and potentially causes a future air shipment delay.

Recognize the cost of chaos

Late spec changes and last-minute origin flips may seem harmless when planning a new sourcing strategy. In practice, they cause rework, schedule slips and emergency freight. Waste increases, emissions go up and paperwork drifts away from what is actually shipped. The real cost becomes clear weeks later.

Instead, focus on stable programs backed by disciplined change control. Keep core components, such as raw material tracing, constant and run revisions through a formal gate. Use statistical process control at sewing and finishing to catch variations while they’re still fixable. Predictability isn’t boring; it’s a margin.

The lesson: Fewer, larger programs with clear improvement paths outperform many one-off efforts. Predictable processes allow teams to choose slower, more deliberate modes and maintain balanced capacity. Chaos results in freight in the sky and defects in the cartons.

What apparel executives can do now

To make these five aspects of apparel operations more accessible, consider the following:

Consolidate ownership: Assign trade, sustainability and sourcing to a single operating leader responsible for specifications and schedules. Link incentives to three outcomes: on-time ocean departures, landed cost versus planned costs, and clean audits without heroics. When one person owns the system, finger-pointing decreases and speed improves.

Reduce variation: Minimize the number of fabrics, trims and processes used across programs. Standardization decreases documentation errors, stabilizes quality and allows design to concentrate on silhouette and color instead of re-engineering chemistry each season. The result is fewer surprises and quicker approvals.

Buy evidence once: Replace patchwork spreadsheets with a single workflow that captures production data, quality control checks and custody records at each handoff. When the trail is integrated into the process, “prove it” becomes a matter of searching, not a crisis situation. Your most trustworthy sustainability message is accurate paperwork that withstands sampling.

Pre-wire options: Use dual-source critical yarns, qualify a second dyehouse and map out tariff scenarios so product and paperwork move together when rules change. Keep commercial terms ready to avoid the need for a new legal review under pressure. Optionality is cheapest when implemented early.

Measure what matters: Track on-time ocean rate, rework percentage, airfreight incidents and audit exceptions. Improve these quarter by quarter, and the rest, such as cost, carbon and credibility, will follow. These four metrics show whether integration is real or just for show.

The through-line

Trade and sustainability are the same production reality seen from different desks. Plan them together, and you avoid duplicate spending, cut down on last-minute fixes and build a supply base that keeps its promises.

Perform the unglamorous work diligently. Use stable specifications, dependable partners, clear documentation and ensure the results appear where they matter most. Fewer line stops, fewer delays, steadier profit margins and goods arriving as scheduled.

That’s the standard. If your process can pass a random Tuesday sampling audit and stay on track, the system works. If not, fix the system — not the story.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-10-22 10:00:002025-10-22 18:08:255 ways to streamline sustainable apparel operations in a time of tariffs

Startup Electra is building a Colorado demonstration facility that will produce 500 tons of low-carbon iron annually, backed by a $50 million grant from Breakthrough Energy and corporate contracts with Meta, Nucor, Toyota Tsusho and Interfer Edelstahl Group.

The 130,000-square-foot facility in Jefferson County is scheduled to open by mid-2026. It will also benefit from an $8 million state tax credit, the maximum amount available under the Colorado Industrial Tax Credit Offering, which has allocated up to $168 million through 2032 for projects that reduce manufacturing energy loads.

Nucor, the largest U.S. steel producer, which uses largely recycled scrap, will buy some of Electra’s iron. Electra also has contracts with two big steel distributors, Toyota Tsusho and Interfer Edelstahl Group, as well as other companies that Boulder-based Electra declined to name. Social media company Meta will buy the environmental attribute certificates related to Electra’s production, which it can use to claim emissions reductions related to data center construction.

The corporate contracts were crucial for the $50 million grant commitment by Breakthrough Energy Catalyst, which funds first-of-a-kind manufacturing projects to help early-stage companies build stronger commercial cases.

“We like to fund projects that derisk technology and move it up the curve,” said Mario Fernandez, head of Breakthrough Energy Catalyst.

Tough economics

Electra uses a low-temperature process to refine iron ore — one that relies on chemistry and renewable electricity rather than a blast furnace fired with coke, a carbon-heavy form of coal. The steel industry, where much of this iron is used, contributes almost 8 percent of global emissions.

Startups like Electra and established players such as ArcelorMittal are working on low-carbon or near-zero steel, but progress has been slow because of the furious pace of construction in countries like China and India and an onerous tariff landscape.

Electra has raised $214 million, not counting the recent grant, from investors including Breakthrough Energy’s venture arm and the Amazon Climate Pledge Fund, which has invested in low-carbon cement and steel to help decarbonize data center construction. (The company will be featured in an Oct. 29 session about “Scaling Low-Carbon Steel” at Trellis Impact 25 in San Jose, California.)

Several buyer coalitions have formed to send early buying signals: both General Motors and Ford Motor, for example, have committed to shifting some of their procurement to favor low-carbon steel.

A lot more supply is needed to meet those promises. It takes at least 1.5 tons of iron to make steel the conventional way, and far less, about 0.60 tons, for steel produced using an electric arc furnace, the process that Nucor uses. A typical U.S. steel plant produces close to 2 million tons annually.

Electra’s initial production at this site wouldn’t fill the construction needs of a hyperscale data center, which might require as much as 20,000 tons. Toyota Tsusho, part of the Toyota Group, plans to sell Electra’s iron for automotive use, while Interfer will target other speciality applications. Electra is also exploring how its iron might be used in magnets and batteries.

The goal at Electra’s site in Jefferson County, near Denver, is to calibrate the company’s processes and test the purity of its product. “We are on track, and this is an important step,” said Kellyn Blossom, head of policy and communications at Electra. “We are hitting our marks and feel confident that we will meet this demand.”

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-10-21 16:00:002025-10-21 18:08:25Why Nucor and Meta are supporting a new low-carbon iron factory

More companies that provide rayon, lyocell and modal to fashion brands are sourcing less from ancient and endangered forests, according to the nonprofit Canopy. Although the vast majority of cellulosic fibers are still spun from virgin materials, some of the biggest producers have been quickly adopting forest-friendly and circular materials.

Seventy percent of companies making semi-synthetic, cellulose-based fibers now exhibit green practices that reduce pressures on forests, according to the10th Hot Button report by Canopy, issued Oct. 16. Fifty four percent of fiber producers that the group tracked have reached the nonprofit’s favorable green rating, with 59 percent offering material traceability.

There has been notable progress over the past decade. Canopy has classified 21 companies as green, up from zero in 2016. And in that time, the number of apparel product lines made from next-gen, preferable sources of manmade cellulosic fibers rose to 16 from none.

Canopy uses this annual report in part to help brands make informed sourcing decisions, in line with its mission to save some of the hundreds of millions of trees felled for fashion each year. The Vancouver nonprofit works with 950 companies to protect forests and biodiversity in apparel, packaging and other industries.

A long way to go

And yet there’s a long way to go to advance circularity in rayon and other manmade cellulosic fibers (MMCFs). Although sourced from wood, plants or and waste, semisynthetics involve chemical and mechanical processing.

The use of recycled materials for such fibers is still rare, although it grew to 1.1 percent in 2024 from .7 percent a year earlier, according to the latest Materials Market Report by Textile Exchange.

Such textiles represent only 6 percent of the global fiber market, according to Textile Exchange. It found that fibers approved by Forest Stewardship Council (FSC) or other certification made up as much as 70 percent of cellulosic fiber market share.

“When we can pull these levers to build demand for those sorts of fibers, the world is better off,” said Forest Stewardship Council U.S. President Sarah Billig.

Who’s doing what

Tied for the top honors in the Hot Button report are Lenzing of Austria, responsible for nearly 13 percent of the worldwide production of manmade cellulosic fibers, and Tangshan Sanyou of China, which makes 9 percent. They are followed by Aditya Birla of India, which supplies almost 16 percent of global volumes.

Such early adopters are also working toward circularity goals, including using less wood and boosting next-generation production by 2030. For example:

Tangshan Sanyou in July started working with textile-to-textile recycler Circ on next-generation lyocell.

The fourth company on the list, Jilin Chemical Fiber, in May began producing Reboocel fiber made from FSC-certified bamboo and bamboo recycled from furniture.

Xinxiang Chemical (Bailu Group) in the spring launched pilot production for recycled viscose.

Other progress includes the rise of textile-to-textile material Circulose, which rose from startup Renewcell’s ashes in Sweden. More brands, such as Reformation, are working its pulp into their collections.

In addition, in February recycling startup Circ launched Fiber Club, a collaboration with Fashion for Good and Canopy. Birla Cellulose, Arvind Limited and Foshan Chicley have joined the effort to push circular manmade cellulosics, along with brands Bestseller, Eileen Fisher, Everlane and Zalando.

Canopy rates companies according to sourcing, conservation, innovation, traceability and other factors. The new report added chemical management to reflect participation in the Zero Discharge of Hazardous Chemicals program.

What needs work

Canopy calls on companies to scale up next-gen materials from crop and textile waste to reduce pressure on forests for virgin pulp.

That said, some smaller fiber companies that employ more advanced circularity practices are struggling. Kelheim Fibres of Germany entered bankruptcy last year. Formosa Chemicals & Fibre of Taiwan is set to fold, and American rayon maker Enka appears to be on the brink of closing.