Google is investing an undisclosed sum in Energy Dome, a startup developer of long-duration battery technology that pairs with solar, wind and other intermittent renewable sources to provide clean power around the clock.

Energy Dome’s CO2 Battery uses liquid carbon dioxide to store electricity as it is generated. When the power source shuts off, the gas expands, running turbines to release energy to the grid. The initial edition of the technology can dispatch 20 megawatts for up to 10 hours. A future version would provide five times that capacity, according to the company’s founder and CEO, Claudio Spadacini.

Google plans to support “multiple” commercial deployments of Energy Dome’s technology — already being used commercially in Sardinia, Italy — the company said in a July 25 blog post. Generally, these installations would be sited near solar and wind facilities. “Solar is very suitable and quite predictable,” said Spadacini.

Google didn’t disclose the locations that would be touched by the new partnership, and it declined further comment about terms of the relationship.

Strong commercial potential

“Long-duration energy storage has the potential to commercialize much faster than some of the other advanced clean energy technologies in our portfolio,” said Google energy strategists Ainhoa Anda and Michelle Chang in the blog. “This means we can use it in the near term to help the electricity system grow more flexibly and reliably, alongside other tools we’re developing, such as data center demand response.”

Energy storage deployments are expected to grow 35 percent for 2025, with a projected 94 gigawatts of additional capacity, according to researcher BloombergNEF. Currently, the most dominant technology for stationary applications related to renewable energy are lithium-ion chemistries.

The price of that technology is appropriate for applications requiring less than four hours of backup electricity during peak demand hours but is tougher to justify for long-duration applications, said Sam Jaffe, principal analyst at consulting firm 1019 Technologies. The artificial intelligence buildout offers one compelling use case.

“The data center boom is coming, and that is an ideal application for longer duration storage paired with solar,” said Jaffe. “You could do a completely renewable data center that way.”

Innovation: Using CO2 to reduce CO2

Energy Dome’s technology involves a tent-like structure resembling an enclosed sports center that needs a lot of space: 10 acres for the small version of the battery. Still, that’s less than 10 percent of the space in a typical solar-plus-storage installation, Spadacini said.

Competitive approaches include flow batteries, which use electrolytes to offer increased capacity, hydrogen fuel cells and pumped hydropower. The U.S., for example, has at least 100 gigawatts of pumped hydro, much of it located next to nuclear sites.

One advantage of Energy Dome’s technology is the well-established supply chain of equipment for liquid CO2. “We are not dependent on made-in-China products,” said Spadacini. That makes the technology eligible for some of the incentives offered under the One Big Beautiful Bill Act.

One challenge will be making sure that Energy Dome’s systems are kept leak-free. “CO2 is a very small molecule and will want to escape,” Jaffe said.

The backstory

Energy Dome was founded in 2019 with seed funding. The Italian startup announced an $11 million Series A raise from 360 Capital and Barclay’s in November 2021, and has raised more than $135 million in all.

The company employs about 90 people, with a small U.S. office in Cambridge, Massachusetts. Founder Spadacini, a mechanical engineer and serial entrepreneur, has also been involved with startups focused on biogas and geothermal applications.

Google is Energy Dome’s first publicly announced corporate contract. Engie is the startup’s partner in Italy. The company’s first U.S. contract is with utility Alliant Energy, which plans to use Energy Dome’s technology for a storage project that can keep 18,000 Wisconsin homes online for up to 10 hours.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-08-04 21:57:172025-08-06 18:08:57This Google-backed startup makes bbatteries that last up to 24 hours

The opinions expressed here by Trellis expert contributors are their own, not those of Trellis.

The artificial intelligence revolution is driving energy demands that could reach 400 terawatt-hours by 2030, up from fewer than 100 terawatt-hours in 2020. What makes this moment particularly consequential isn’t just the scale of these energy demands, but how they’re reshaping the landscape of corporate climate commitments for companies outside the tech elite.

The new energy pecking order

The “Magnificent Seven” — Apple, Microsoft, Amazon, Alphabet, Meta, Tesla and Nvidia — account for roughly one-third of the S&P 500’s total market capitalization. These companies possess something that most other corporations don’t: the financial resources and strategic leverage to secure dedicated clean energy sources for their operations, no matter the cost.

When the world’s most valuable companies purchase their way to carbon-free electricity through long-term nuclear contracts, they create a two-tiered system where a company’s sustainability efforts become increasingly correlated with market capitalization.

The grid under siege

Energy demand for data centers could increase by as much as 165 percent by 2030, according to a Goldman Sachs analysis. Most electricity consumed by data centers currently relies on fossil fuels. While the MAG-7 secures clean energy through private agreements, the broader electrical grid is being strained to accommodate the growing demands of everyone else.

This creates a cascading effect that undermines the sustainability efforts of virtually every other industry. In Northern Virginia, for example, the region’s concentration of data centers has forced utilities to keep fossil fuel plants online to meet demand. When utilities must fire up additional gas plants to meet AI-driven electricity demand, the carbon intensity of the entire grid increases, making it more difficult for all grid-connected companies to achieve their emissions reduction targets.

Consider the math: Companies are still committing to Net Zero but only reducing emissions by 30 percent on average by 2030, falling short of the 43 percent reduction required to limit global warming to 1.5 degrees Celsius. These already insufficient results become even more challenging when the electrical grid itself becomes more carbon-intensive due to AI’s energy demands.

When utilities must fire up additional gas plants to meet AI-driven electricity demand, the carbon intensity of the entire grid increases,

Proponents of AI expansion will tell you the technology’s potential to drive efficiency gains could offset energy consumption. But that argument represents optimistic forecasting and ignores the immediate realities of deployment: training AI models consume thousands of hours of electricity and generate hundreds of tons of carbon dioxide. It’s like the Jevons Paradox but applied to AI: improvements in efficiency lead to increased consumption — not conservation.

Other companies find themselves in a difficult position. They face rising electricity costs as utilities struggle to meet AI-driven demand, limited access to clean energy sources that are increasingly locked up in long-term contracts with tech giants, and stakeholder pressure to maintain ambitious climate commitments. The result is a growing gap between stated intentions and achievable outcomes.

This is particularly acute for manufacturing companies, which typically operate on thinner margins than tech firms and cannot easily absorb increases in energy costs. When the price of electricity rises due to grid strain, and when clean energy sources become less available due to tech sector capture, these companies face a choice between seeking to achieve their climate commitments and maintaining their competitiveness.

Facing reality

The uncomfortable truth is that we’re witnessing the emergence of a bifurcated approach to corporate sustainability. Companies with sufficient capital and strategic importance can secure clean energy sources and maintain credible climate commitments. Everyone else must compete for increasingly scarce and expensive clean electricity while operating in a grid environment that is becoming more carbon-intensive due to AI-driven demand.

Recent innovations such as in-memory computing, optical data transmission and more efficient AI models such as China’s DeepSeek, which reportedly consumes 10 to 40 times less energy than comparable models, demonstrate that AI’s energy consumption is not immutable. Yet the dominant approach remains focused on scaling up energy supply rather than optimizing demand.

For non-tech-giant companies, the path forward requires several strategic adjustments:

Sustainability commitments must be recalibrated to reflect grid realities. Companies will have trouble achieving agreed to science-based targets on a grid that’s becoming more carbon-intensive due to factors beyond their control. This doesn’t mean abandoning climate goals but rather setting targets that account for systemic constraints.

Companies must invest more heavily in direct energy efficiency measures and on-site renewable generation. When clean grid electricity becomes less available, the next best option is to reduce dependency on the grid altogether.

Corporate climate advocacy must shift toward systemic solutions rather than individual commitments. The Science Based Targets initiative aims to commit 20 percent of the global economy to fully validated science-based targets by 2025, but these targets become meaningless if the underlying energy infrastructure cannot support them.

Broader implications

What we’re observing in the AI energy boom is a microcosm of broader challenges in addressing climate change through market mechanisms. When critical resources — in this case, clean electricity — become scarce, they flow to the highest bidders rather than the most socially beneficial uses. Hyperscalers like Google and Amazon aren’t villains in this story; they’re rational actors responding to market incentives. But their rational behavior creates externalities that undermine the climate commitments of virtually every other company.

As AI’s inevitable development continues, energy implications must be addressed at a systemic level rather than left to individual corporate procurement strategies. This requires policy interventions to ensure that clean energy deployment keeps pace with AI-driven demand and that access to clean electricity isn’t determined solely by purchasing power.

The companies driving AI development have the resources to reconcile these tensions for themselves through private energy agreements. For everyone else, the path forward requires acknowledging that sustainability in the age of AI will be more challenging, more expensive and more dependent on systemic solutions than we’ve been willing to admit.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-08-04 10:00:002025-08-04 18:09:03How the AI energy reckoning will reshape corporate climate commitments

Kids wear out onesies, footed PJs and T-shirts at an exhausting rate. (For parents, anyway.) And like most of fashion, children’s clothing hasn’t typically featured the circular economy staples of durability, reuse and recycling.

But with the industry facing a sustainability reckoning — and big brands having been slow to capitalize on expectations that used children’s apparel sales will grow 11 times faster than fashion overall — Carter’s, H&M Group and Gap Inc. are taking varied approaches to address the waste, chemicals and carbon footprints of their kidswear.

They’re doing so in a fast-expanding ecosystem fueled by increasingly concerned parents:

More than one-third of parents plans to buy back-to-school products with sustainability attributes for their kids, according to a 2024 Deloitte survey.

To support their net zero goals, validated by the Science-Based Targets initiative, the following best-selling names in kidswear focus less on product end-of-use. Instead, they’ve made headway on their materials footprints through things such as organic-cotton certifications and investment in textile recycling startups. Here’s a snapshot of how three best-selling children’s brands approach these efforts:

Carter’s

The 160-year-old Atlanta company holds a roughly one-fifth market share for children’s clothing, including its namesake brand and Osh Kosh B’Gosh. With 1,200 U.S. stores and wholesale partnerships with Amazon and Walmart, its sales reached $2.8 billion last year.

Carter’s sustainability strategy centers around safety, durability and sourcing, according to Anu Piduru, senior director of sustainability.

By this fall, 99 percent of its clothing will have Oeko-Tex 100 certification. That label reflects testing of every part of a garment — including zippers, buttons, prints and labels— for the absence of 1,000 chemicals of concern, such as PFAS, bisphenol-A and heavy metals. This exceeds most regulatory requirements.

Carter’s maintains a restricted substances list for finished products and is rolling out the same for manufacturing, in alignment with respected standards.

The company’s small organic-cotton Little Planet line has taken off over the past four years, according to Piduru, “The biggest draw is the sustainable aspect, the certified organic cotton and the recycled materials that go into those products,” she told Trellis. Little Planet meets the Global Organic Textile Standard, which ensures organic fibers with “clean” chemistry.

The company wants to use cotton — which makes up 70 percent of its fiber mix — that is 100 percent sustainably sourced by 2030, enabled in part by the Better Cotton standard.

In May, Carter’s rebooted its KidsCycle takeback initiative; what was once as a mailback program has now expanded into (some) stores. In the most recent full year of the program, Terracycle helped Carter’s downcycle 22,467 pounds worth of products into bedding and sports equipment.

According to Piduru, Carter’s is still trying to understand its customers’ perception of brand sustainability and circular business models. That’s especially important, she said, because kidswear production cycles aren’t at a fast-fashion pace. “We don’t just kind of turn and burn through these designs,” Piduru said.

Carter’s hasn’t jumped into branded resale, partly because so many informal and third-party networks exist for people to keep kids’ clothes in circulation. For example, tens of thousands of Carter’s items sell each year on eBay, ThredUp and elsewhere.

“As a mom myself, I know that children’s clothes in general are getting probably more used or used by more people than adult clothing is,” Piduru said. “You buy one shirt as an adult, and you might wear it once and donate it once, but I’ve got kids’ clothes that have been handed down to us by nieces and nephews and siblings.”

Eventually, though, “Circularity in childrenswear makes sense given its shorter lifecycles,” said Tasha Lewis, a North Carolina State University professor of human sciences who researches sustainability in fashion.

Gap Inc.

The San Francisco company, which had $15.1 billion in revenue last year, sells one-fifth of all baby clothes in the U.S., according to IBIS World. Relevant brands for the under-18 set include Gap Baby, Gap Kids, Old Navy and Athleta.

Gap Inc. got rid of PFAS in 2023, ahead of state regulations. It keeps restricted substances lists both for finished products and manufacturing.

Leaning heavily on natural fibers, Gap reached 98 percent cotton from “sustainable sources” in 2024, toward a 100 percent goal this year. That includes Better Cotton-certified material. Forty percent of its polyester is recycled, toward a 45 percent goal for 2025. As with H&M, however, it’s unclear, exactly where such preferable materials appear within children’s clothing.

“As the resale revolution continues to gain momentum, participating in re-commerce is not only good for our planet, but good for business,” said Mark Breitbard, Gap Inc.’s president of specialty brands, in 2020.

H&M Group

Stockholm-based H&M Group, with 4,338 stores in 2024, accounts for 5-9 percent of the kids’ apparel market, according to Future Market Insights.

It’s not easy to determine exactly how much of the privately held group’s $24 billion in annual sales last year came from its juvenile offerings, but in its H&M retail stores, non-adult clothes appear to take up at least 10 percent of floor space.

Although a fast fashion mainstay, the company seeks to become fully circular. “That means reducing waste and emissions across the value chain, and creating new business models that keep garments in use longer,” said CEO Helena Helmersson said in 2023.

As for resale, the H&M Pre-Loved line has since 2023 offered used clothing for all ages in partnership with ThredUp. H&M is also a majority owner of the European secondhand site Sellpy.

Meanwhile, H&M is also investing in recycled materials. For example, last year it co-launched startup Syre. It also recently revived its support of cotton-recycling startup Circulose and and has invested in lab-grown cotton startup Galy.

In 2024, 89 percent of the materials across H&M’s brands were recycled or “sustainably sourced,” toward a goal of 100 percent by 2030. All of its cotton is recycled, organic or otherwise sustainably sourced through programs such as Better Cotton. Ninety-four percent of its polyester is recycled, toward a 100-percent goal for 2025.

H&M was ahead of the curve 30 years ago in publishing its restricted materials list. The brand went PFAS-free more than a decade ago. It has demonstrated leadership in chemical management within its supply chain, backed up with well-respected third-party standards. However, like Gap, H&M has not focused on consumer-visible certifications such as OEKO-TEX.

One exception: its small collections of infant apparel with C2C Gold Certification from 2023. These organics could be composted at home, according to the standard overseen by the Cradle to Cradle Products Innovation Institute.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-08-01 17:14:002025-08-05 18:08:47How Carter’s, H&M and Gap are making kidswear more sustainable

Many sustainability experts say judicial action is one of the most powerful tools civil society can use to drive sustainability outcomes in the near term, according to a global survey by Trellis data partner by GlobeScan in collaboration with ERM and Volans. This view has gained significant traction in light of the International Court of Justice’s historic advisory opinion on climate change issued in July, which declares that a clean, healthy and sustainable environment is a fundamental human right.

The ICJ’s landmark ruling affirms that countries have legal obligations to prevent environmental harm under international law. Crucially, the ruling finds that states failing to meet their climate commitments are in breach of international law and that they must cooperate to achieve concrete emissions reduction targets. This reframes climate action as a legal imperative rather than a policy preference, and elevates the strategic importance of litigation, legal systems and accountability mechanisms in the global sustainability agenda.

Alongside legal avenues, experts also point to education and leadership development, policy advocacy and media scrutiny as top civil society strategies to accelerate progress. In contrast, less structured or symbolic approaches, such as NGO campaigns, public protests or boycotts are seen as less impactful in achieving systemic change.

What this means

The ICJ’s advisory opinion may be a turning point for climate justice. Although technically not legally binding, it sends a powerful message that could reshape international climate negotiations and jurisprudence. For the more than 3,000 pending climate lawsuits globally, the ICJ’s affirmation of legal obligations offers fresh momentum and potential legal precedent for holding governments and corporations accountable.

For businesses and policymakers, this means climate litigation risk is rising. The advisory opinion may also influence the tone of negotiations at COP30, fueling increased pressure for enforceable targets and climate finance for vulnerable countries.

Looking ahead, legal action may no longer be a last resort and could instead become a primary lever in the sustainability toolbox. Companies would be wise to monitor evolving legal norms, proactively align with international commitments and embed climate risk into their governance and strategy before courts and public pressure force their hand.

Based on a survey of 844 sustainability practitioners across 72 countries conducted April-May 2025.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-08-01 10:00:002025-08-01 18:08:36See you in court: Judicial action is key driver of sustainability outcomes

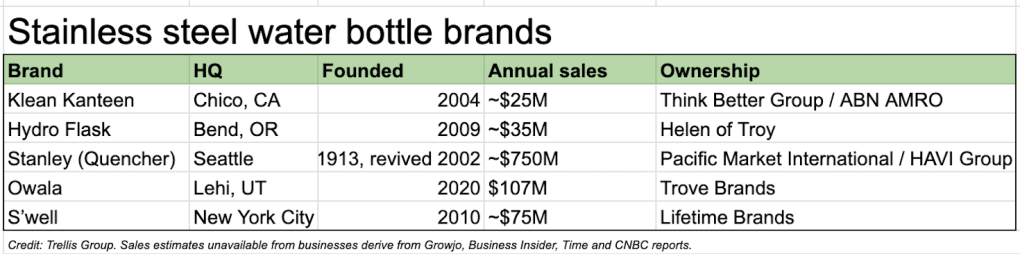

Klean Kanteen helped to popularize plastic-free, reusable water bottles, weathering two decades by focusing on durable products rather than chasing aggressive growth. Ideals of serving “people, planet and profit” have helped the certified B Corporation endure recent challenges including tariffs that are uniquely hurting smaller businesses. In addition, the brand is adapting from a 2024 buyout and competing against copycats and the persistence of single-use plastic.

“We maintain by staying core to who we are and why we originally started, and not deviate too much from that,” said Global Product Manager Hunter Shoop.

Standing against plastic

Privately held Klean Kanteen, which does not release sales figures, is navigating its share of the growing, $1.45 billion global market for stainless steel bottles. That will reach $2.08 billion by 2032, according to Data Bridge Market Research.

That said, with two supplier plants in China, Klean Kanteen has found the erratic tariff policies of the Trump administration a challenge. “They’ve jumped from single digits to triple digits, so it’s a pretty large impact on the business,” Shoop said. So far, Klean Kanteen has capped price increases to about $2 on certain products. Its 27-ounce bottles now list for $21.95.

The tariffs have not hurt Klean Kanteen’s sustainability efforts, though, which include working with suppliers to monitor their renewable energy usage and carbon footprints, according to Shoop.

Nevertheless, the Chico, California, business continues to swim upstream in its mission to provide alternatives to single-use plastic:

Disposable plastic water bottle sales skyrocketed by nearly 3,000 percent between 1997 and 2021 in the United States, according to the Container Recycling Institute.

People toss more than two-thirds of the 86 billion bottles sold annually.

That $4.34 billion worldwide plastic bottle market will hit $6.46 billion in 2032, according to Fortune Business Insights.

Northern California roots

A father, son and daughter took over Klean Kanteen 19 years ago from Robert Seals, a Northern California sculptor who shaped the initial steel vessel. He had made Klean Kanteen a fixture at green festivals, music fairs and grocery co-ops. As some of the first stainless steel refillable options on the market, they appealed to consumers who considered single-use plastic water bottles severely uncool. (Shout out to my early-aughts model from Solar Festival in Hopland, California.)

The company had a headstart against mainstream fears over the health harms of drinking out of plastics, such as cancer, infertility and poor brain development. That gained momentum in 2008, when Walmart yanked plastic bottles containing toxic bisphenol-A from its shelves. Klean Kanteen also rode the wellness wave as bring-your-own-bottle hydration became the norm for gym rats and elementary schoolers.

In February 2024, the family-owned company allowed a third party to take over a controlling stake. That English investor, Think Better Group, is a mission-focused brand-holding group for sustainable products. It’s part of ABN AMRO SIF of Amsterdam, a $571 million institutional impact fund. Its other holdings include Ecoriginals diapers, Colonna Coffee and Minor Figures beverages.

“They’re bringing in some optimization and things like that, but for the most part, we still get to run independently, and it’s business as usual,” Shoop said.

The staff of roughly 40 people often sees the co-owner siblings, Michelle Kalberer and Jeff Cresswell, as the first in the building each day. “Their desks are literally out in the open in the middle of our offices,” Shoop said.

Pursuing certifications

“Everything that we do is around sustainability, trying to drive our footprints down, monitoring and measuring with third-party certifications,” Shoop said.

For instance, Klean Kanteen aligns its climate emissions reductions with those of the Science-Based Targets initiative, although it’s not formally pursuing validation. The goals include a 58.8 percent drop in emissions from Scopes 1 and 2 from a 2016 baseline by 2030, and a 30 percent Scope 3 reduction compared with 2019. The company is also Climate Label Certified.

By contributing 1 percent of gross sales to the 1% for the Planet program, Klean Kanteen has supported 135 nonprofits over 20 years. It will reach $5 million in giving this year, according to Caroleigh Pierce, who leads the company’s partnership and community engagement efforts.

Prizing durability

Making long-lasting, durable products that can be repaired and ultimately recycled underpins Klean Kanteen’s materials and design choices.

“When at all possible, we try and make our products so they can be repaired,” Shoop said, “or making sure that they could also be disassembled for proper end of use.”

A single-wall, non-insulated bottle remains Klean Kanteen’s best seller, especially in Europe. However, insulated bottles are increasingly popular, and an oven- and microwave-safe reusable food box also sells well.

The company has spruced up bottle designs with colors and patterns, customizing caps for different beverages, but it hasn’t wildly diversified its product lineup.

Strong sales of replacement kits for lids and their silicone gaskets reflect that customers are buying in to Klean Kanteen’s circularity strategy. How-to cleaning and maintenance videos encourage lifetime use.

Materials and safety

In addition to the circular-economy focus of durability, Klean Kanteen introduced 90 percent recycled steel in all products several years ago.

“There are other brands that are starting to dabble a little bit here, a little bit there, but we made a commitment to jump all in,” Shoop said. The company worked with the raw steel manufacturer, not just the sourcing managers.

That recycled content, certified by Intertek, includes reclaimed steel from sources such as industrial equipment and even used kitchen appliances and tableware. The steel, a rust-proof alloy of 18 percent chromium and 8 percent nickel, doesn’t leach chemicals or flavor the water it holds, according to the company.

In addition, Klean Kanteen introduced a Klean Coat finish several years ago to prevent color chipping and dents. The finish is applied by spraying a powder of electrically charged polyester resins that is then heat-cured.

The company uses the GreenScreen for Safer Chemicals standard to ensure the coating is free of lead, BPA and phthalate chemicals.

Unlike aluminum bottles, stainless steel bottles have no plastic lining. Instead, an electropolish finish smoothes out microscopic irregularities inside each bottle.

Klean Kanteen uses a chemical hazard analysis for its bottle components and packaging as well.

Its focus on chemical safety is reflected in partnerships with the Environmental Working Group and the Breast Cancer Fund.

Small hangtags for retail displays comprise much of Klean Kanteen’s packaging footprint, although plastic bags wrap products that are shipped. The company tried biobased plastic packaging but reverted to recycled petroleum plastic, which was more likely to be recycled.

Lots of sales happen online, including from Amazon. That said, “We’re not losing sight of our roots and where we started,” Shoop said. “So we’re still in those organic grocery stores and the smaller chains.”

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-07-31 21:14:002025-08-01 18:08:43How Klean Kanteen steeled the water bottle market

The potential impacts of unchecked climate change — flooding, drought, resource scarcity, even lawlessness — are certainly familiar to Trellis readers. But seeing such catastrophes actually unfold provides a deeper perspective, highlighting how individuals and societies might cope — or not! — under the strain of environmental collapse.

With that in mind, we’ve curated nine films that professionals in the sustainability field are bound to enjoy — or at least enjoy hate watching. Are we suggesting a screening for your next offsite? Not necessarily. Would we show up? We look forward to the e-vite.

Mad Max

For those unfamiliar with this Mel Gibson-before-he-lost-it classic from 1979, a quick catch-up: Max is a former policeman navigating a lawless society in a world ravaged by ecological collapse and resource scarcity. At its core, Mad Max asks what happens when communal guardrails vanish and violence reigns, ultimately standing as a warning about the fragility of society. Gritty and iconic, a little funny and a lot terrifying, the movie once held the Guinness World Record for the highest box-office-to-budget ratio.

Waterworld

Upon its release in 1995, Waterworldwas the most expensive movie ever made (budget: $175 million) — and a box office flop. (Then again, so was The Wizard of Oz.) But even if you’re not a Kevin Costner fan, this action-packed thriller is worth a watch. Set in a future in which the ocean has submerged most of the planet, the film follows a mutant survivor who encounters all sorts of obstacles as he seeks dry land. In a nutshell: Resources are scant, refuge is elusive and the argument for fighting rising sea levels at all costs is clear and convincing.

WALL-E

As charming as it is sobering, Pixar’s WALL-E (2008) follows the eponymous robot as he dutifully tries to clean up an Earth destroyed by waste. After stumbling upon remnants of human life, he’s taken on an eye-opening galactic journey. With minimal dialogue —but a lot of beeping and booping — and powerful imagery, this family-friendly multiple Oscar winner delivers a harsh message about climate change in a gentle manner suitable for even the youngest viewers.

The Age of Stupid

On a planet that lies in ruins, a lone archivist reflects on why humans failed to act when they still had the chance. This 2009 blend of documentary footage, dramatized accounts and animation draws a clear line between today’s decisions today and tomorrow’s consequences, reminding viewers that the window for meaningful change is finite. In the words of one Financial Times reviewer, The Age of Stupid offers “the wisdom of hindsight, today.”

Snowpiercer

After a failed climate intervention leaves the world frozen, the last survivors find shelter aboard a perpetually moving train segregated by class. When the lowest rung of humans decides to take over the elite’s front car, things take a revolutionary turn. Snowpiercer uses its dystopian setting to explore a present truth: that climate disasters often deepen existing societal divides. Visually striking and thematically bold, the 2013 film challenges viewers to question who should hold the power when the world stops turning. Wrote The New York Times in its review: “Planetary destruction and human extinction happen a half-dozen times every summer. It’s rarely this refreshing, though.”

Don’t Look Up

Two astronomers discover an impending, literally Earth-shattering disaster and set about spreading the word — only to be met with apathy and disdain. The star-studded cast (Leo!, JLaw!, Streep!) of Don’t Look Up (2021)adroitly dramatizes the consequences of ignoring such urgent real-life issues as climate change denial and media sensationalism, wrapping a now-or-never call to action in an edge-of-your-seat story.

How to Blow Up a Pipeline

This Independent Spirit Awards winner (for best editing) from 2022 follows a group of young activists as they plan to sabotage fossil fuel infrastructure. Through the lens of radical action, How to Blow Up a Pipeline communicates the gravity of the climate crisis, particularly as perceived by our youth. Inspired by understandable real-world frustration with institutional inaction, it raises controversial yet compelling questions about civil disobedience, violence and environmental justice.

The End We Start From

Set in a near-future London submerged by catastrophic flooding, The End We Start From (2023) follows a new mother fighting for her baby’s survival. As infrastructure collapses, her journey turns into a personal tale about the quiet ferocity of motherhood. The movie received nine nominations at the 2023 British Independent Film Awards, a testament to its emotional depth and atmospheric storytelling.

Flow

In thisanimated, wordless odyssey from 2024, a cat navigates another post-apocalyptic, submerged world. Crisis, in the movies at least, often makes for strange bedfellows, and along the way our protagonist finds companionship in a dog, a lemur, a capybara and a bird. Together they drift past drowned cities and tangled ruins, the destruction stunningly rendered. Flow, infused with feelings of cooperation and resilience, earned an Oscar, the first Latvian movie to do so.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-07-31 16:23:002025-07-31 18:08:269 meaningful movie nights for the sustainability minded

When RMI surveyed carbon market participants over the past couple of years, the non-profit heard tales that will be familiar to anyone who has navigated the ecosystem’s confusing array of document and data types. Project developers reported spending up to 60 percent of their time dealing with requests for data. Buyers said due diligence could take as long as 18 months.

In July, the organization unveiled its solution: an open-source framework designed to “bring structure to the vast universe of carbon credit data.”

The potential benefits of RMI’s Carbon Crediting Data Framework (CCDF) are already evident in a pilot catalogue of carbon credits developed by Centigrade, a startup that is partnering with the non-profit. On display are climate projects ranging from fuel-efficient cookstoves in Guatemala to forest conservation in Mississippi. Potential buyers and other users can click through to a wealth of information, presented in standardized form for each project. Data points include number of available credits, estimated price and ratings from third-party agencies.

Hundreds of data fields

Underneath the hood of Centigrade’s system is a framework based on at least 570 fields, grouped into categories and sub-categories. The fields were chosen by RMI’s Carbon Markets Initiative team and integrate methodologies from major registries, including Verra and Puro.earth; quality criteria from the Integrity Council for the Voluntary Carbon Market; and templates for suppliers, such as those developed by Frontier, a coalition of carbon removal buyers.

Widespread adoption of the framework would bring multiple benefits, said Bonnie Lei, an RMI principal. Project developers could make a single set of data available for potential buyers, eliminating the duplicative effort of replying to several different sets of questions. And buyers could assemble candidate projects in a data room for easy comparison.

Making it easier for buyers to assess credit quality is a focus of the project, added Lei. Free-to-access databases of credits already exist, including one developed by the Climate Action Data Trust, a stakeholder initiative founded by the World Bank and others. But the CCDF is designed to extend these projects by providing additional data.

“You really need to be able to go into these sets of fields that get into understanding the emissions components of the credit,” said Lei. “As well as the social, environmental dimensions, which we believe are really important and distinguishing for credits.”

One schema to rule them all

To realize the vision of a unified data framework, the CCDF’s backers now need to persuade market players to back it. One wrinkle here is that RMI’s framework is not the only game in town. Sixteen schemas have been submitted to the Carbon Data Open Protocol (CDOP), a stakeholder initiative designed to develop a common data framework. The project is co-chaired by RMI, which has submitted the CCDF alongside the others. Lei said she expected the different options to be inputs into a single framework that will be published in stages, with the first release planned for Climate Week NYC in September.

If and when the CDOP committee reaches an agreement, adoption will still be a challenge. “There are real costs in terms of coordination and implementation to pulling off this sort of standardization,” said Grayson Badgley, a research scientist at CarbonPlan, a nonprofit that analyzes climate solutions. “Everyone already has their systems in place and I’d imagine changing things comes with all sorts of edge cases and risks. First and foremost, the incentives and benefits of standardization need to outweigh those costs.”

It’s also worth noting that data standardization does not inevitably mean that project developers will share all the information needed to fully evaluate projects. “It’s equally important that everyone can access the actual project and credit data itself,” said Badgley. “That would help make sure that everyone — buyers, sellers, researchers — has the ability to study and evaluate the performance of both individual projects and the market as a whole.”

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-07-31 05:00:002025-07-31 18:08:26RMI takes aim at the messy data that plague carbon markets

Shengyuan Su, whose position as Zendesk’s director of sustainability was eliminated as part of broad layoffs in February, has taken on a new role as director of sustainability disclosure for Western Digital.

Su reports to Jackie Jung, the computer storage company’s vice president of global operations and strategy, corporate sustainability and transformation.

In a LinkedIn post, Su said her responsibilities include promoting Western Digital’s strategy and impacts, ensuring regulatory compliance and helping embed sustainability metrics and practices into all aspects of its business.

Western Digital, which reported revenue of $13 billion for its 2024 fiscal year, has committed to become net zero for its direct operational emissions and its purchased energy (Scope 1 and 2) by 2032. It aims to cut emissions for its direct materials by 20 percent by 2030, compared with a 2024 baseline.

As of its latest update, Western Digital reported an absolute reduction for Scope 1 and 2 of 36.3 percent.

During her two-and-a-half years with Zendesk, Su established the company’s relationship with Frontier, the $1 billion carbon removal buyers initiative. She was also responsible for instituting a Zendesk procurement policy requiring suppliers to set science-based targets for emissions reductions by 2027.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-07-30 20:11:002025-07-31 18:08:27Former Zendesk sustainability lead lands at Western Digital

Nearly every week brings another brand partnership, factory blueprint or financing deal related to a polyester recycling startup. The space is crowded with young companies seeking to weave together a circular economy that pushes virgin polyester to the margins.

In a few short decades, polyester has displaced cotton as the dominant fiber. It’s found in nearly two-thirds of new fashions. Because it’s made with cheap fossil fuel byproducts, however, the apparel industry’s emissions shot up 7.5 percent in 2023 after a modest dip, according to a June report by the Apparel Impact Institute. And as a result, the industry accounts for almost 2 percent of all the world’s climate emissions.

Brands striving to reduce that impact, along with its regulatory and operational risks, plan to procure more recycled and “next-generation” materials. So far, only 12.5 percent of polyester comes from recycled sources, 99 percent of which begins as bottles rather than textiles, according to the Textile Exchange.

The Textile Exchange Materials Directory highlights clusters of synthetic fiber and textile production. Credit: Textile ExchangeSource: Samsara Eco

It’s no easy feat to court partners in a new, waste-based supply chain within the fragmented textile industry. To begin with, a startup needs an efficient technology to transform unwanted fabrics into something new. It must also procure and sort castoff garments or factory clippings from third parties. Once the buttons, trims and zippers are removed, the material needs to be recycled into a raw output, such as polyethylene terephthalate (PET) pellets. Yet another partner spins that into fiber, which someone else turns into a textile for a brand.

The final leg in this process: efficient factories. “Ramping to full capacity, which they must operate close to if they are to at least break even, is the big challenge,” said Marcian Lee, an analyst with Lux Research.

Textile recycling executives insist that there’s room for multiple players to spin old plastic threads into valuable textiles. Here’s how five of them are seeking to bring a textile-to-textile recycling system to life.

Circ

Circ is building a $500 million plant in northeastern France. Scheduled to open in 2028, it would be the largest industrial polycotton recycling operation.

Many synthetic recycling startups say they accept textile blends, including polyester-cotton, to produce material for fresh polyester fibers. Circ distinguishes itself by recycling the cotton, too.

“You’re really maximizing the economic value of what’s in that starting material,” Conor Hartman, Circ’s chief operating officer, told Trellis in May. “We’ve taken polycotton originating material and made it into beautiful lyocell products and beautiful polyester products.”

Circ’s process recovers polyester, as well as cotton from polyester-cotton blends. Credit: CircSource: Samsara Eco

Circ’s recycled cellulosic lyocell appeared in a small collection last month from Zalando, which is an investor, as are Patagonia and Inditex. Circ recently inked deals with fiber producers, too, including China’s Tanshan Sanyou and Portugal’s Selenis.

Earlier this year, Circ kicked off Fiber Club, a collaboration to scale recycled fibers that Bestseller, Eileen Fisher, Everlane and fiber producers support. Such bridge-building follows the Circ-Ready community launch of partners a year ago.

Virginia-based Circ has attracted $76.6 million of investment, the most recent coming in 2023 via a Series B raise of $25 million.

Ambercycle

Ambercycle has partnered with Reformation, Arc’teryx and Gap’s Athleta as well as important textile and polyester companies in North America, Europe and Asia, including Shenghong Holding Group and Zhejiang Huilong New Materials of China.

In January, the startup secured an offtake agreement to replace about 20 percent of Danish brand Ganni’s polyester usage. That follows a three-year, 70-million-euro offtake agreement with Inditex in 2023 and another binding deal with brand Mas.

“We’ve tried to piece together the pathway to get to this commercial scale, because the challenge with us and really everyone in this space is that, out the gate, the competition with existing fibers is pretty significant,” CEO Shay Sethi told Trellis in June.

Ambercycle is developing an enzymatic recycling feature that would allow a multi-fiber output, enabling brands a “one-stop shop” if they want specific blends of, say, polyester, nylon or spandex, according to Sethi.

Last year, Taiwan’s Shinkong Synthetic Fibers provided $10 million toward a commercial plant for Ambercycle, expected to open in 2026. Ambercycle, whose pilot plant has been running in Los Angeles since 2022, has raised $56 million in its 10 years.

Sethi envisions an industry that balances both centralized operations and regional production. “With textile waste, for better or worse, there’s no shortage anywhere you look,” he said.

Reju

With offices in Paris, Reju piggybacks on its Dutch parent Technip Energies, which counted $6.9 billion in revenues last year. The umbrella company’s resources in engineering and chemicals include polyester production.

European Union rules that require brands to take responsibility for their textile waste provide a boost, but Reju is eyeing “regeneration hubs” elsewhere, too. It hooked up with Goodwill and Waste Management last fall to lay a foundation in North America.

Reju uses IBM’s VolCat technology, short for volatile catalyst. “We’re dealing with known chemistry here,” CEO Patrik Frisk told Trellis in May. “Part of what makes polyester so easy for the textile industry is, first of all, the infrastructure for it has been thoroughly developed over the last 70 or 80 years.”

That frees up Reju to build out its circular system, according to Frisk, former CEO at Under Armour. Despite its problematic origins and contribution to microplastic waste, the material is endowed with useful properties and thus here to stay, he said. “We’re able to take away all the stuff that’s bad, and create new again.”

By giving the waste a second life, Reju can potentially design materials that shed fewer microfibers, Frisk added.

Samsara Eco recycled textiles to make the peach Lululemon Swiftly top of nylon 6,6 and the purple Anorak polyester jacket. Credit: Samsara ecoSource: Samsara Eco

Samsara Eco

With machine learning, Samsara Eco customizes enzymes that “eat” polyester. Last year, it proved it can do the same for nylon 6,6. The result appeared in a long-sleeve Lululemon top. In June, the startup established a decade-long offtake agreement, vying to provide potentially one-fifth of Lululemon’s overall fiber portfolio.

In addition to creating a $25 million R&D hub in Jerrabomberra, Australia, Samsara Eco is working with Israeli nylon producer Nilit on a recycling plant to open next year in Southeast Asia, home of partner waste suppliers.

“But that will only be the first of our facilities where we’re talking closely with polymerization partners in Europe and in North America as well across better packaging and fashion,” CEO Paul Riley told Trellis last winter.

Samsara Eco has raised $107 million. It aims to give new life to 1.5 million tons of plastics annually by 2030. That’s less than half of 1 percent of global plastic production each year, leaving plenty of room for multiple recyclers, Riley suggested.

“We’re looking at infinite recycling, true circularity across fashion and packaging,” he said, “and an important thing to note is that there is no difference between our molecule and a fossil fuel molecule. We tap straight into the supply chain.”

Syre

Syre in June touted strategic deals to supply Gap, Target and Houdini Sportswear with its chemically recycled polyester, which it says carries only 15 percent of the CO2-equivalent footprint of the virgin standard. Gap alone would use 10,000 metric tons of Syre’s output annually.

First, though, Syre has to break ground on the 12 commercial scale plants it originally announced for late 2026.

Syre is colocating a pilot plant in North Carolina with a Selenis polyester production facility. It has the ambition to bring “gigascale” plants to Vietnam and Iberia in the next few years. “This is the start of the great textile shift,” Syre CEO Dennis Nobelius told Trellis in June.

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-07-30 16:44:002025-07-30 18:09:37These 5 companies hope to spin old polyester threads into fashion gold

The opinions expressed here by Trellis expert contributors are their own, not those of Trellis.

As a professor and author focused on corporate sustainability, there’s one question I’m asked more than any other: Which companies are getting it right?

I wish I could tick off a list of role models or whip out a cheat sheet of organizations that are checking all the boxes. But I can’t — and won’t — because not only is asking that question missing the point, but it’s also actively dangerous.

Our obsession with performance

While the intention behind the question is positive, the outcome is a quagmire of confusion, in which we obsess over being perfect at the expense of making progress. Our obsession with sustainability poster children illustrates how much we confuse context with performance. It also stops us learning from practices that actually work, many of which are forged by companies in the most controversial and troubled sectors that wrestle daily with the thorny side effects of simply doing business.

The trouble with our performance obsession became clear to me when Patagonia founder Yvon Chouinard handed over ownership of the firm to a nature-based charity in 2022. After a few hours of social media celebration, commentators began to note that the structure would facilitate tax avoidance, that the business still relied on synthetic fabric and that employees hadn’t been given a stake.

This dilemma is also featured in Trellis’ Chasing Net Zero series, which documents the progress that companies are making toward their climate progress — and how they stack up against their peers.

If handing over a profoundly successful operation to a philanthropic cause will do nothing to keep the critics at bay, then it’s time to ask what our hunt for sustainable companies is actually achieving. Are we trying to drive innovation, or raise the bar just slightly? Should we prioritize deep change in a few areas or broad, superficial gestures everywhere, such that the strategy winds up as “everything is material”?

The ultimate paradox in responsible business is that best and worst practices are often found side-by-side in the same industry.

If you were to rely on sustainability conferences and media reporting, you’d get a warped impression of which sectors have the most advanced approaches on any particular issue. For example, there are frequent press exposes of horrific practices in the supply chains of apparel and food companies. And child labor and deforestation in the cocoa supply chain in West Africa and sexual abuse on sugar plantations in India. You’d get the impression that these sectors have the most appalling, neglectful supply chain oversight out there. Is there considerable truth to this? Yes. Does it mean that practices are better in other sectors, particularly those with less scrutiny? Absolutely not.

The reality is that if you want to find the most advanced thinking on supply chain oversight, this will also be found in the food and apparel sectors. Because we care greatly about what we eat and what we wear, these sectors are most exposed to stakeholder scrutiny. So it’s in apparel and food companies that you’ll find leading practices on traceability, transparency, living wage efforts, smart decarbonization, supply chain finance and more. The ultimate paradox in responsible business is that best and worst practices are often found side-by-side in the same industry. Sometimes even in the same factory.

Reputational risk can be a funhouse mirror

If you’re looking to campaign against companies that negatively affect human rights, a great place to start is in the mining and social media sectors. Mine operators can subject local communities to noise, pollution, relocation, unpredictable job prospects and the potential for life-threatening operational disasters.

Meanwhile, social media companies undermine our mental health, polarize us and encourage screen addiction, to say nothing of online exposure to torture and hate speech, and the impact on those tasked with keeping this content from the public eye.

Does this mean such companies lack expertise on human rights? Not at all. In fact, if I want to find the most advanced thinking on business and human rights issues, the first place I’d look is in these sectors. Because of the scale of friction these companies face, at least some of them must hire experts to help them manage and calibrate these risks. That’s why you’ll find mining companies leading on collective decision-making in communities, just as others trample on community rights every day. And you’ll find substantive and thoughtful efforts within some social media companies to tackle online discourse alongside profound carelessness. Both best and worst practice, in the same sector.

The truth is most discussions of corporate responsibility implicitly assume that absence of controversy affirms good performance. But the reality is that the company most likely isn’t highly exposed to the issue or stakeholder group in question. Reputational risk is held as a linear accountability mechanism, when in reality it is a funhouse mirror. If you doubt this, a recent OECD report on ESG metrics found that only 2 percent of all ESG metrics account for the external context — the degree of exposure to an issue.

The wrong poster children

No company manages all stakeholders with the same level of intensity and effort, and companies simply don’t develop expertise in the absence of friction. But rather than acknowledging this, and learning from those at the forefront of a particular challenge, we’ve encouraged generic messaging around “commitments to stakeholders,” PR-driven goals set in a vacuum, and an exhausting cycle of promotional activity and activist teardowns.

Our favorite poster children may not be those making the best effort to tackle a particular issue, but companies that can create attractive business upside from an issue, or even use their promotional efforts to distract attention from more fundamental externalities become sustainability darlings. For example, it’s common for chief sustainability officers at big technology companies to solely focus on on renewable energy data centers, and strenuously avoid talking about the policy influence their employer wields globally in an effort to stop any regulation of their core externality — their impact on individual and group human cognition.

Good-faith efforts

We’ve spent far too long in a fraught and arcane quest to score good versus bad, and it’s getting us nowhere. We’ve tried reducing corporations to a single ESG score, only to find it’s not so easy to put the trade-offs between negative and positive externalities into a metaphorical ledger. We’ve tried highlighting examples of “good practices,” only to wind up cherry-picking the most convenient, least messy examples — ones that flatter our desire for neat, happy stories rather than the real, difficult work of transformation.

What if the primary question that matters is whether a company is making a good faith effort to tackle the negative impacts that are core to how it makes money? What if progress over time is a far better way to evaluate corporations than whether it can be considered “green” or “inclusive” overall? What if we valued progress over time — real, demonstrable, progress — over snapshot judgments about which companies are “role models”? And what if, in our rush to make business “good,” we’ve forgotten that the best any business can do is to make itself better — day after day, step by step, in a world full of contradictions, trade-offs and hard choices?

https://sustainable-future.org/wp-content/uploads/2025/03/cropped-trellis_favicon_180x180.png3232sustainablefuturehttps://sustainable-future.org/wp-content/uploads/2024/06/Untitled-design-117-300x94.pngsustainablefuture2025-07-30 10:00:002025-07-30 18:09:38Beyond ‘good’ and ‘bad’: How to measure corporate sustainability